Singapore Cold Chain Logistics Market: By Technology (Vapor Compression, Blast Freezing, Evaporative Cooling, Programmable Logic Controller, Cryogenic Systems, Other Technologies); Temperature Technology (Chilled (0°C to 15°C), Frozen (-18°C to 0°C), Deep-frozen (< -18°C)); Solution (Cold Chain (Warehouse/storage (Refrigerated Warehouse, Controlled Atmosphere Storage)), Cold Chain Transport (Refrigerated Trucks, Air Freight, Marine Transport), Automated Temperature Type Handling, Refrigerated Packaging); Storage Capacity (Small-scale (Up to 1,000 MT), Medium-scale (1,000-5,000 MT), Large-scale (Above 5,000 MT)); Industry (Food and Beverages, Fruit and Vegetable, Meat and Seafood, Dairy and Frozen Dessert, Bakery and Confectionery, Ready-to-eat Meal, Chemical, Pharmaceuticals, Medical, Others)—Market Size, Industry Dynamics, Opportunity Analysis and Forecast for 2026–2035

- Last Updated: 05-Feb-2026 | | Report ID: AA02261700

Market Scenario

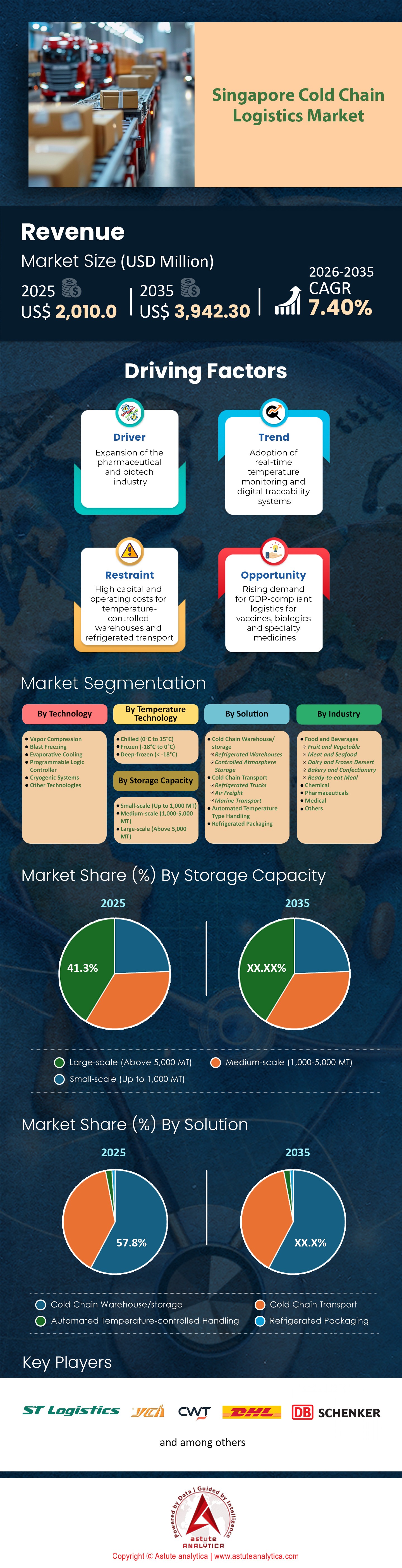

Singapore cold chain logistics market is valued at approximately USD 2,010.0 million, with a projected trajectory to breach USD 3,942.30 million by 2035, growing at a CAGR of 7.40% during the forecast period 2026–2035.

Key Market Highlights

- By technology, vapor compression segment holds highest share 42.67% in the Singapore cold chain logistics market.

- By temperature technology, chilled (0°C to 15°C) segment holds highest share 50%.

- By solution, cold chain warehouse/storage segment holds highest share 57.76%.

- By storage capacity, large-scale (>5,000 MT) segment holds highest share 41.3%.

- By industry, food & beverages segment holds highest share 78.09%.

The Singapore cold chain logistics market is currently navigating a pivotal "super-cycle" of modernization. This growth is not organic, it is engineered. The convergence of Singapore’s "30 by 30" food security mandate, the operationalization of the Tuas Mega Port, and the post-pandemic cementation of the island as the primary pharmaceutical distribution hub for APAC has created a perfect storm for high-value logistics.

However, the market is bifurcated. There is an oversupply of aging, low-specification cold rooms (20+ years old) that bleed energy and fail to meet modern SS 668:2020 standards. Conversely, there is a chronic shortage of Prime Logistics Assets—facilities with >12m ceiling heights, modern ammonia/CO2 cooling systems, and ASRS (Automated Storage and Retrieval System) integration.

- Key Investment Thesis: The profit pool in Singapore cold chain logistics market is shifting from "storage volume" to "complexity management." Stakeholders who invest in specialized capabilities—specifically Halal-certified hubs, GDP-compliant Pharma zones, and Green Mark Platinum infrastructure—will command rental premiums of 40-60% over general industrial peers.

To Get more Insights, Request A Free Sample

Food Security & "30 by 30": How Is Government Policy Driving Infrastructure in the Cold Chain Logistics Market?

The "30 by 30" goal (producing 30% of nutritional needs locally by 2030) is a massive infrastructure driver.

- The Shift: Traditional cold chains were designed for Import -> Store -> Distribute.

- The New Model: Farm -> Pre-Cool -> Store -> Distribute.

- Local high-tech farms (e.g., vertical farms, coastal fish farms) require Source-Based Cold Chain.

- The Gap: Most local farms lack industrial-grade "Pre-Cooling" facilities (Hydro-coolers/Vacuum coolers) to remove field heat immediately.

- Opportunity: The Agri-food Cluster Transformation (ACT) Fund in the Singapore cold chain logistics market provides substantial grants for logistics providers to partner with farms to build on-site cold storage, reducing spoilage rates (which currently sit at ~10-15% for leafy greens).

Critical Challenges: What Are the Bottlenecks Limiting Growth?

JTC Land Lease Decay:

Industrial land in Singapore is owned by JTC. Most plots are on 20 or 30-year leases.

The Problem: Building a high-spec automated cold store in the Singapore cold chain logistics market is a 20-year ROI project. If a plot has only 12 years left on the lease, the bank will not finance the construction, and the operator cannot recoup the investment. This leads to "Infrastructure Stagnation" where operators sweat old assets rather than upgrading.

Energy Volatility:

Singapore relies on imported Natural Gas. Global fluctuations impact electricity tariffs. For a cold chain operator, a 20% hike in tariffs can wipe out the net profit margin for the year.

The "Freezer Work" Stigma in Singapore Cold Chain Logistics Market:

Singaporeans generally refuse to work in -20°C environments. The reliance on foreign labor is absolute. Tightening border policies directly threaten operational continuity.

Ecosystem Analysis: How Does Singapore’s "Dual-Engine" Logistics Model Work?

To understand the Singapore cold chain logistics market, it is imperative to recognize that Singapore does not operate like a standard consumption city. It operates on a Dual-Engine Model:

Engine 1: The Domestic Resilience Grid

Singapore imports >90% of its food. The domestic engine is driven by high-frequency, lower-volume distribution to supermarkets (NTUC FairPrice, Cold Storage), HORECA (Hotels, Restaurants, Catering), and an exploding Direct-to-Consumer (DTC) quick-commerce sector. This engine demands "Last-Mile" efficiency and central kitchens located near population centers (e.g., Pandan Loop, Senoko).

Engine 2: The Global Transshipment Hub

This is the high-margin engine of the Singapore cold chain logistics market. Wherein, the country handles over 38 million TEUs annually. A significant fraction of this is reefer (refrigerated) cargo. High-value perishables (e.g., Australian Wagyu, Cultured Meat, French Dairy, Norwegian Salmon) and biomedical products land in Singapore not for consumption, but for Break-Bulk and Value-Added Services (VAS)—re-labeling, re-packaging, and freezing—before being re-exported to Indonesia, Vietnam, and Thailand.

- Strategic Analysis: The "Transshipment Engine" is immune to local recessionary pressures but highly sensitive to global trade routes. The current shift of maritime traffic from Keppel/Tanjong Pagar to the Tuas Mega Port is reshaping the logistics map, moving the center of gravity West.

Market Size & Forecast: What Do the Numbers Say About Growth Verticals in Singapore Cold Chain Logistics Market (2026–2035)?

| Segment | 2026 Est. Value (USD) | 2035 Forecast (USD) | CAGR | Key Drivers |

| Food & Beverage | $1.02 Billion | $2.62 Billion | 0.112 | "30 by 30" local production; Premiumization of diets in SEA. |

| Pharmaceuticals | $0.55 Billion | $1.8 Billion | 0.158 | Vaccine hubs; Clinical trial logistics; Aging population. |

| Chemicals/Others | $0.28 Billion | $0.9 Billion | 0.135 | High-tech semiconductor materials requiring temperature control. |

The "Value Over Volume" Trend:

While Food & Beverage accounts for the highest volume (tonnage), the Pharmaceutical sector contributes disproportionately to profit margins of the Singapore cold chain logistics market. Handling a pallet of frozen chicken yields a low single-digit margin; handling a pallet of oncology drugs (requiring -80°C storage) yields margins upwards of 25-30%. The forecast indicates that by 2030, Pharma cold chain revenue will rival Food revenue, despite significantly lower volume.

Regulatory Deep Dive: How Do SS 668:2020 and SFA Requirements Impact Barriers to Entry?

Singapore Standard (SS) 668:2020: Cold Chain Management of Chilled and Frozen Foods. This standard, which replaced TR 49 and CP 95, is the definitive barrier to entry for new players in the Singapore cold chain logistics market.

Critical Components of SS 668 Impacting Operations:

- Part 1 (General Requirements): It mandates a documented Cold Chain Management System (CCMS). Operators cannot just "turn on the AC." They must provide evidence of annual calibration of all sensors, preventative maintenance logs, and a "Recall Procedure" specifically for temperature-abused goods.

- Thermal Mapping (The "Hot Spot" Rule): Before a warehouse is licensed, it must undergo 24-48 hours of thermal mapping (empty and loaded) to identify "hot spots." Data loggers in the Singapore cold chain logistics market must be permanently installed at these specific worst-case points.

- The "Unbroken Chain" Mandate: Handover points are critical. The standard dictates that goods must not be left on loading bays. Facilities must have Dock Shelters and Inflatable Seals to ensure the truck effectively becomes part of the cold room during loading.

- SFA Enforcement: The Singapore Food Agency (SFA) links the Food Storage Warehouse License to compliance. Any "Break in Cold Chain" (BICC) incident that leads to spoilage must be reported. Repeated failures lead to license suspension, effectively killing the business in the Singapore cold chain logistics market.

Niche Market Opportunity: Why is Halal Cold Chain Logistics a High-Growth Vector in Singapore?

Singapore is positioned as a global Halal Hub, and Halal Logistics.

The Integrity Challenge:

Muslim consumers are increasingly aware that a product is only as Halal as its supply chain. If Halal beef is stored in the same cold room as pork, cross-contamination (spiritual and physical) risks occur.

MUIS (Majlis Ugama Islam Singapura) Certification Standards:

To capture the Singapore cold chain logistics market, logistics providers must obtain the Halal Certification for Storage Facilities.

- Ritual Cleansing (Sertu): If a facility previously held non-Halal items, it must undergo Sertu—washing with water mixed with clay/soil—witnessed by MUIS auditors.

- Segregation: It is not enough to wrap pallets differently. There must be a physical barrier (wall or partition) or dedicated cold rooms.

- Dedicated Transport: Halal goods typically require "Halal-only" trucks to prevent cross-contamination during the last mile.

- Market Winner: Yusen Logistics and YCH Group have established dedicated Halal hubs in Tuas, allowing them to service the export market to the Middle East and Indonesia (the world’s largest Muslim population).

Pharma & Life Sciences: How Does the "Control Tower" Model Drive GDP Compliance in the Singapore Cold Chain Logistics Market?

Singapore is home to manufacturing facilities for Pfizer, GSK, Sanofi, and AbbVie. The logistics requirement here is governed by Good Distribution Practice (GDP) standards for Medical Devices (GDPMDS) and Medicinal Products.

The "Control Tower" Concept:

Top-tier providers (DHL, Kuehne+Nagel) operate "Control Towers" in Changi. These are 24/7 command centers that monitor active shipments globally.

Active Containers: Usage of Envirotainer or CSafe units (containers with internal batteries and compressors).

The "60-Minute" Rule: At Changi Airport (Coolport), the tarmac time (time from aircraft touchdown to temperature-controlled facility) is benchmarked at under 60 minutes. This speed is a critical KPI in the Singapore cold chain logistics market that allows country to outrank regional rivals like Bangkok or KL.

The growth area in the Singapore cold chain logistics market is Cell & Gene Therapy (CGT) logistics. These require cryogenic storage (-150°C to -196°C) using liquid nitrogen dry shippers. Few players in Singapore have this capability, making it a "Blue Ocean" niche.

Rental Rate Analysis: How Much Does Cold Storage Cost in Tuas vs. Changi?

Stakeholders need to understand the "Cold Premium."

| Zone | Asset Type | Rental Rate (SGD psf/month) | Trend |

| Tuas / Jurong West | Ambient Warehouse | $1.50 - $1.90 | Stable |

| Tuas / Jurong West | Cold Storage (Fitted) | $2.60 - $3.40 | Rising (Tuas Port Demand) |

| Changi / East | Ambient Warehouse | $2.00 - $2.50 | High Demand |

| Changi / East | Cold Storage (Fitted) | $3.80 - $4.80+ | Very High (Pharma Premium) |

| Central (Pandan) | Cold Kitchen / Last Mile | $4.00 - $5.50 | Scarcity Value |

Cost Breakdown:

The rental premium covers the Capex of fit-out (~$150−200 psf for insulation/refrigeration) and the depreciation of equipment. However, Utility Costs are usually borne by the tenant. In Singapore, electricity can constitute 35-45% of the total operating cost for a cold storage facility, significantly higher than the global average due to tropical ambient temperatures and imported energy.

Competitive Landscape: Who Are the Key Players Domineering the Singapore Cold Chain Logistics Market?

The market is stratified into three distinct tiers:

Tier 1: Global Integrators (Pharma & MNC Focused)

- Kuehne+Nagel: Dominates the pharma/healthcare sector with its intense GDP compliance framework.

- DHL Supply Chain: Strongest network; heavy investment in the "Advanced Regional Center" (ARC).

- DB Schenker: Strong presence in the airport logistics park (ALPS).

Tier 2: The "National Champions" (Asset Heavy)

- YCH Group: The pioneer of "Supply Chain City." Their strength lies in their proprietary "The Last Mile" (TLM) tech and deep ASEAN connectivity.

- CWT Integrated: Owners of massive cold storage footprint (e.g., CWT Cold Hub). They focus on commodity volumes, wine, and general food.

- Tee Yih Jia: Originally a food manufacturer (Popiah skins), now a cold chain giant with massive automated freezers in Senoko.

Tier 3: The Disruptors (Last-Mile & E-Comm) in the Singapore Cold Chain Logistics Market

- Ninja Van (Ninja Cold): Disrupting the "Less-Than-Truckload" (LTL) chilled market.

- Pickupp / Lalamove: Aggressively entering the on-demand refrigerated courier space.

Future Trends: What Are the "Next Big Things" in Singapore Cold Chain Logistics Market?

Green Cold Chain & LNG Cold Energy Harvesting:

Singapore imports LNG (Liquefied Natural Gas) at -162°C. Currently, this "cold energy" is dumped into the sea during the regasification process.

Currently, several projects are underway (SLNG) to capture this cold energy to freeze air for district cooling or directly power cold storage facilities on Jurong Island. This drastically reduces the carbon footprint and opex.

Solar-Powered Warehousing:

With the carbon tax rising (targeting $50-80/ton by 2030), installing solar roofing is becoming standard to offset the energy intensity of compressors.

Q-Commerce Micro-Hubs:

Singapore cold chain logistics market is witnessing the emergence of "Cloud Freezers"—small, automated cold rooms located inside HDB (public housing) car parks or shopping mall basements, serving as forward stock locations for 15-minute grocery delivery apps.

Segmental Analysis of the Singapore Cold Chain Logistics Market

By Technology, Vapor Compression Control the Largest Market Share

The dominance of vapor compression technology, holding a 42.67% share, is structurally enforced by Singapore’s rigorous energy standards under the "Singapore Green Plan 2030." As of 2025, the National Environment Agency (NEA) has tightened Minimum Energy Efficiency Standards (MEES) for industrial water-cooled chilled water systems, which account for 90% of industrial cooling electricity consumption in the country. This regulatory pressure compels cold chain operators to adopt advanced vapor compression systems that utilize low-Global Warming Potential (GWP) refrigerants.

Major industrial landlords like JTC Corporation have integrated these high-efficiency systems into new developments, such as the Bulim Square facility completed in October 2025, to meet the Building and Construction Authority’s (BCA) Green Mark Platinum standards. The technology’s scalability ensures it remains the primary engine for maintaining temperature stability across Singapore's sweltering tropical climate, making it indispensable for logistics players seeking compliance and operational cost reduction.

By Temperature Technology, Chilled Segment (0°C to 15°C) As Need for Critical Infrastructure for National Food Security is On the Rise

The chilled segment’s commanding 50% share of the Singapore cold chain logistics market is directly tied to Singapore’s "30 by 30" food security goal, which aims to locally produce 30% of nutritional needs by 2030. According to the Singapore Food Agency’s (SFA) 2024 statistics, the nation diversified its food import sources to 187 countries/regions to mitigate supply chain risks, necessitating robust chilled storage for perishables like eggs, leafy vegetables, and dairy.

Retail giants like NTUC FairPrice have expanded their chilled infrastructure; their Fresh Food Distribution Centre (FFDC) now utilizes precision cooling zones to handle volume surges, a necessity as local egg production rose by 13% in 2024 due to farm upgrades. This segment acts as the logistical backbone for the "farm-to-fork" freshness promise, supporting both the massive volume of daily imports and the burgeoning output from local high-tech agri-food clusters.

By Storage Capacity, Large-Scale (>5,000 MT): Industrial Hubs Driving Economies of Scale

The large-scale storage is controlling 41.3% market share of the Singapore cold chain logistics market. The dominance is mainly underpinned by the consolidation of logistics operations into mega-hubs to maximize land-use intensity. In 2024, SATS Ltd, through its Coolport facility, demonstrated the efficacy of large-scale aggregation by handling record volumes of transshipment perishables, leveraging automated storage and retrieval systems (ASRS) that are only viable at capacities exceeding 5,000 MT.

The completion of JTC’s Bulim Square in October 2025, adding over 110,000 sqm of industrial space, exemplifies the shift toward massive, multi-tenanted logistics ecosystems. These facilities allow major players to amortize the high costs of automation and cold chain integrity monitoring.

Furthermore, with Micron Technology’s $24 billion investment in 2026 for new manufacturing facilities, the demand for large-scale, industrial-grade temperature-controlled warehousing has intensified, cementing this segment’s supremacy.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Industry, Food & Beverages: Sustaining Consumption via Import Diversification Networks

The food & beverages industry is holding a 78.09% share of the Singapore cold chain logistics market and dominance is necessitated by Singapore’s 90% food import reliance. The SFA’s 2024 report highlights that despite global disruptions, the volume of food imports remained resilient due to diversified sourcing, requiring agile cold chain solutions for F&B distribution. In 2025, FairPrice Group’s sustainability report revealed that their logistics network saved over 1,095 tons of fresh produce through efficient cold chain management, underscoring the segment's critical role in waste reduction.

The expansion of central kitchens and last-mile delivery services for F&B retail has further deepened this dominance. With the population’s increasing consumption of temperature-sensitive products like premium meats and dairy, logistics providers prioritize F&B capabilities, ensuring this segment captures the lion's share of investment and infrastructure development.

To Understand More About this Research: Request A Free Sample

Strategic Case Studies: Real-World Examples of Excellence in the Singapore Cold Chain Logistics Market

Case A: Sankyu Tuas Hub (The Heavyweight)

Sankyu’s investment in Tuas is a strategic bet on the port shift. Their facility is designed to handle dangerous goods (DG) / chemical temperature control—a niche within a niche. By locating near the port, they reduce the "drayage" cost (trucking containers from port to warehouse), offering a total landed cost advantage to chemical MNCs.

Case B: ESR-REIT & The "Asset Enhancement" Strategy

ESR-REIT has been aggressive in acquiring older cold stores and executing Asset Enhancement Initiatives (AEI).

They acquire a low-yield facility, strip it to the frame, install modern ammonia-glycol cooling systems, increase the power supply, and re-lease it to a tenant like FairPrice Group on a long lease. This highlights the value of retrofitting in a land-scarce market.

Top Companies in the Singapore Cold Chain Market

- A. P. Moller-Maersk A/S (Maersk)

- United Parcel Service (UPS)

- Cushman & Wakefield

- DB Schenker Logistics Company

- DHL Logistics

- MNX Global Logistics

- Yusen Logistics Service

- Pan Ocean

- Americold Logistics LLC

- C.H. Robinson Worldwide

- CEVA Logistics SA

- Lineage Logistics Holding, LLC

- NewCold Coöperatief UA

- Other Prominent Players

Market Segmentation Overview

By Technology

- Vapor Compression

- Blast Freezing

- Evaporative Cooling

- Programmable Logic Controller

- Cryogenic Systems

- Other Technologies

By Temperature Technology

- Chilled (0°C to 15°C)

- Frozen (-18°C to 0°C)

- Deep-frozen (< -18°C

By Solution

- Cold Chain Warehouse/storage

- Refrigerated Warehouses

- Controlled Atmosphere Storage

- Cold Chain Transport

- Refrigerated Trucks

- Air Freight

- Marine Transport

- Automated Temperature Type Handling

- Refrigerated Packaging

By Storage Capacity

- Small-scale (Up to 1,000 MT)

- Medium-scale (1,000-5,000 MT)

- Large-scale (Above 5,000 MT)

By Industry

- Food and Beverages

- Fruit and Vegetable

- Meat and Seafood

- Dairy and Frozen Dessert

- Bakery and Confectionery

- Ready-to-eat Meal

- Chemical

- Pharmaceuticals

- Medical

- Others

FREQUENTLY ASKED QUESTIONS

The market reached USD 2,010 million currently. It will grow to USD 3,942 million by 2035 at a 7.4% CAGR, driven by food security mandates and Tuas Mega Port operations.

The goal to produce 30% of nutritional needs locally by 2030 demands source-based pre-cooling for vertical farms. ACT Fund grants enable logistics firms to build on-site cold storage, cutting spoilage by 10-15%.

Food & beverages hold 78% share due to 90% import reliance and diversified sourcing from 187 countries. Efficient cold chains saved 1,095 tons of produce in 2025, supporting retail giants like FairPrice Group.

Vapor compression commands 42.7% share via Green Plan 2030 energy standards using low-GWP refrigerants. Chilled storage (0-15°C) holds 50% share as the backbone for perishables under the 30 by 30 food security initiative.

Sankyu's Tuas Hub cuts drayage costs near the new Mega Port while handling chemical temperature control niches. Large-scale facilities (>5,000 MT) at 41% share leverage port proximity for transshipment economies of scale.

Pharmaceuticals grow fastest at 15.8% CAGR from vaccine hubs and CGT cryogenic needs (-196°C). Halal-certified and GDP-compliant facilities command 40-60% rental premiums over commodity cold storage.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |